TimCScott on Nostr: Looking for something to read with your weekend morning coffee? Here's an article I ...

Looking for something to read with your weekend morning coffee? Here's an article I wrote earlier this week about US Bonds/Economy since Fed rate cuts.

quoting nevent1q…hwkxA BRIEF LOOK BACK AT US BONDS/ASSETS/BITCOIN SINCE FED RATE CUT (SEP 18 – DEC 31)

TLDR: US Debt Trap – Stubborn Inflation – Hold Bitcoin

Happy New Year! My first post of any real substance on Nostr. I wanted to challenge myself over the Christmas holidays and finally dive into Nostr with the hopes of publishing my thoughts in short article form and engaging with the community. My first few days on here have been very positive. As someone who comes from a small town, I see a lot of similarities to the Nostr community.

There’s not a lot we can concretely predict into the future from a little over 100 days of data, but let’s take a look at where we are at and have some fun.

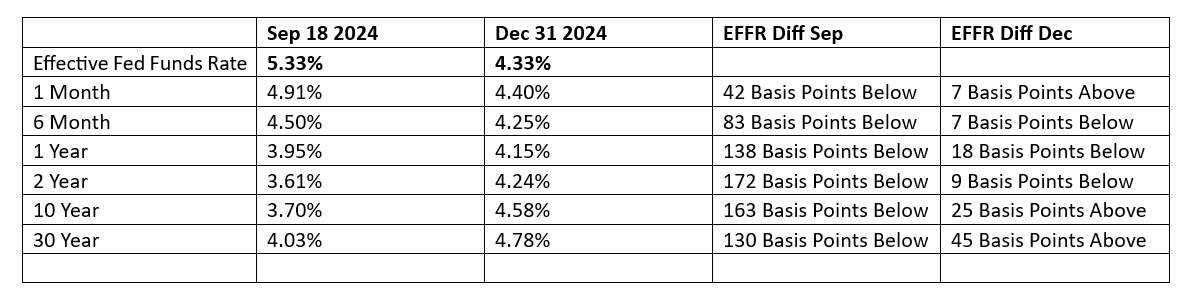

On September 18, 2024 the FOMC started its latest easing cycle and as of December 31st 2024 the effective funds rate has seen 100 basis points in cuts.

Let’s take a closer look at what treasury rates did over this time period and what my opinions are on what we are seeing. IMO Bond rates give the best signal of where things are and where the smartest money in the world thinks things are going.

I take away a few things from this. Effective Fed Funds Rate has eased 100 basis points and the 10 Year yield has risen by almost 100 basis points. The economy is relatively strong, investors aren’t really worried and are still willing to invest their money elsewhere than the bond market. That being said while yields are starting to un-invert and flatten, there is still a lot of uncertainty in the bond market. It’s important to remember the rate cuts have not been because the US is worried about a recession. The US is in a debt trap and deficits to GDP have never been this high. Is now a good time to own long term debt denominated in USD? No, it isn’t… bond rates are clearly signaling that they are not convinced inflation is going away and that future rate cuts are expected to slow. If inflation was to go higher (which seems a reasonable consideration), anything long term denominated in USD loses. I wouldn’t be surprised to see the 10-year yields test 5% again – The last time was in Oct 2023 and was only there for mere minutes. Next time, it might stay above it.

The US Public debt was 35.331T on Sep 18 and increased to 36.150T by Dec 30 (as per treasury.gov), an increase of 819 billion in new public debt in 103 days. This is slightly less bad than some previous reports of 1T in new debt every 100 days. The majority of the issuance during this time period has been in the 2-year and less durations. The smartest Bond holders sold off massive quantities of long dated treasuries during COVID believing prices would fall when yields rose. They were betting taxes would not rise nearly enough to offset deficit spending during the pandemic. They were right – bond holders who stayed put got hosed, experiencing one of the biggest drops since World War I. The US Government stepped in and bought ALL long-term Treasuries issued at times between 2020-2022. When the government finally stopped buying, yields spiked and prices crashed. This dilemma still exists today, just on a smaller scale – the US Government needs to actually demonstrate a commitment of raising taxes or cutting spending for a sustained period. Good luck.

The 30-year mortgage rate has increased from 6.15% on Sep 18 to 7.07% on Dec 31 (as per MortgageNewsDaily). This shouldn’t come as much of a surprise as it is very closely tied to the 10-year yield. Mortgage rates have increased 92 basis points, and the 10-year yield has increased 88 basis points. Mortgage rates north of 6% were perfectly normal pre-2008 – time to get used to it. QE and interest rate repression messed up the mortgage market and will now likely bounce in the opposite direction in the coming years. Owning real estate as an investment doesn’t look good at all in the coming decade IMO.

The price of gold has increased from $2,570.10 on Sep 18 to $2,616.00 on Dec 27 (as per YCharts) up roughly 1.79% during this time period. Gold’s price movements often signal where investors think inflation is going. However notably, the DXY was at 100.6 on Sep 18 and up to 108.49 on Dec 31. This tends to keep prices of gold down. This also feeds back into my premise that the US economy is strong and investors aren’t worried. International investment in the US is very attractive and is being well rewarded at this time.

Bitcoin has performed exceptionally well over this time as well. Rising from $61,649 on Sep 18 to $93,429 on Dec 31 (as per CoinMarketCap) a gain of over 51%. I am pretty biased when it comes to Bitcoin, I am a big advocate and believe everyone should have at least some. It allows you to opt out of the market manipulation and dysfunction created by central planners. Clearly this easing cycle has been very positive for the volatile asset, rising as high as $108,268 on Dec 17th. My core thesis is still that inflation is going to be more persistent than the majority believes. That the 10-year yield will hit 5% again in 2025 and inflation will see an uptick are positive Bitcoin – granted as the community says – everything is good for Bitcoin. All I’ll add is that we are still incredibly early, so many people still have no knowledge of Bitcoin or it’s benefits, there is always work to do.

We’ve barely scratched the shrink wrap of the economic/market data we could have looked at in this post. I wanted to keep this relatively short (was aiming for 500 words – blew past that). If you enjoyed this post, please consider giving it a boost on your Nostr feed. As my friend Deckard Cain would say – Stay awhile and listen. Until next time.

Peace and Love.